Paycheck Take-Home Calculator

Determine your net take-home salary instantly. Enter your wages, pay frequency, and filing status to see federal income taxes, FICA withholding, and optional savings allocations.

Estimated Take-Home Pay

per bi-weekly pay period

Detailed Deductions Breakdown

Select Your State Calculator

State laws vary. Select your state below to include local tax brackets, state-level disability insurance (SDI), and paid family leave (PFL) withholding rules.

Demystifying FICA Withholding Guidelines

FICA taxes are flat payroll contributions split between employees and employers. The Social Security tax consumes 6.2% of your gross pay up to the 2026 limit of $184,500. Wages beyond this ceiling bypass this withholding entirely.

Medicare charges a baseline of 1.45% of gross income with no cap. An additional 0.9% Medicare surcharge applies to earnings exceeding $200,000 (single) or $250,000 (married). Our system dynamically monitors these thresholds based on pay frequency and filing categories.

Pre-Tax Benefits vs. Post-Tax Savings

Leveraging pre-tax benefits allows you to reduce your tax exposure directly. Standard retirement contributions (401k or 403b) lower your federal taxable income base. That portion of your salary escapes current income taxes, though FICA taxes are still calculated from your gross income.

Healthcare premiums, HSA, and Flexible Spending Accounts (FSAs) are qualified under Section 125 cafeteria plans. These premiums are fully tax-exempt, meaning they reduce both federal income tax and FICA tax calculations. Adjusting these allocations inside the advanced settings panel reveals how they lower tax liability while preserving net income.

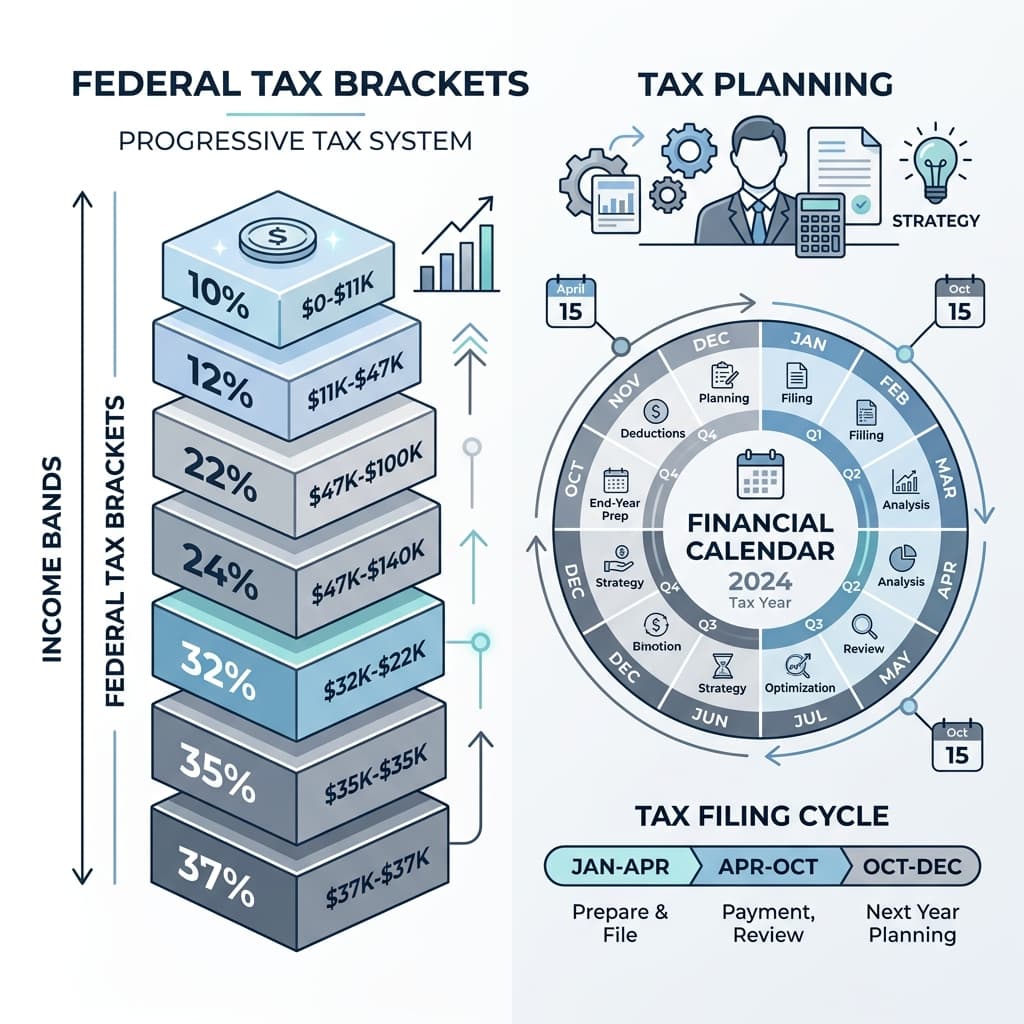

2026 Marginal Tax Brackets Comparison

The progressive tax brackets apply to taxable income after subtracting standard deductions ($16,100 Single / $32,200 Married).

| Tax Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 10% | $0 – $12,400 | $0 – $24,800 | $0 – $17,700 |

| 12% | $12,401 – $50,400 | $24,801 – $100,800 | $17,701 – $67,450 |

| 22% | $50,401 – $105,700 | $100,801 – $211,400 | $67,451 – $105,700 |

| 24% | $105,701 – $201,775 | $211,401 – $403,550 | $105,701 – $201,775 |

| 32% | $201,776 – $256,225 | $403,551 – $512,450 | $201,776 – $256,225 |

| 35% | $256,226 – $640,600 | $512,451 – $768,700 | $256,226 – $640,600 |

| 37% | $640,601 or more | $768,701 or more | $640,601 or more |

How to Manually Calculate Your Take-Home Pay

While payroll software automates check generation, understanding the mathematical sequence underlying each deduction is crucial. This step-by-step framework explains how a paycheck is calculated manually:

Step 1: Determine Gross Earnings

Gross wages represent your total earnings before any deductions. For salaried employees, this is your annual base salary divided by the number of pay periods. For hourly workers, multiply your hourly rate by the total hours worked in that pay cycle.

Step 2: Apply Section 125 Exemptions

Subtract pre-tax medical, dental, and health savings account (HSA) premiums from gross earnings. These are Section 125 deductions and are exempt from both FICA and federal income tax, establishing your adjusted taxable FICA base.

Step 3: Calculate Social Security & Medicare

Multiply your FICA base by 6.2% for Social Security (subject to the $184,500 limit for 2026) and 1.45% for Medicare. If your year-to-date wages cross $200,000 ($250,000 for married couples), apply the additional 0.9% Medicare tax.

Step 4: Subtract Retirement Plans (401k)

Subtract pre-tax retirement contributions (such as traditional 401k or 403b plans) from the remaining gross amount. This reduces your wages for federal income tax calculations, establishing your federal taxable income base.

Step 5: Deduct Progressive Income Tax

Annualize your federal taxable income base, subtract the IRS standard deduction ($16,100 for Single/MFS or $32,200 for MFJ), apply the marginal tax brackets (10% to 37%), and divide the annual tax by your pay frequency.

Step 6: Account for Post-Tax Deductions

Deduct any post-tax benefits such as Roth 401(k) allocations, union fees, or child support orders from your remaining balance. The resulting figure is your net take-home pay, which is direct-deposited into your account.

Net Pay vs. Take-Home Pay: Is There a Difference?

In colloquial terms, Net Pay and Take-Home Pay are used interchangeably. However, in professional payroll administration, there is a minor technical difference. Net Pay refers to gross earnings minus mandatory tax withholdings (federal income tax, state income tax, local tax, and FICA). Take-Home Pay represents the actual final amount you receive after both taxes and optional employee deductions (such as retirement savings, union dues, health insurance premiums, or parking fees) have been processed.

State-by-State Payroll Tax Structures

State income tax (SIT) rules vary significantly, dividing the country into three main categories:

- No State Income Tax (9 States): Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming charge zero state income tax on earned wages. Washington imposes a capital gains tax, but standard payroll is SIT-exempt. New Hampshire does not tax earned wages, but does tax interest and dividend income.

- Flat Income Tax States (10+ States): Arizona, Colorado, Idaho, Illinois, Indiana, Iowa, Michigan, Mississippi, North Carolina, Pennsylvania, and Utah impose a single flat percentage rate on all taxable wages, regardless of total annual earnings.

- Progressive Income Tax States (Remaining States): California, New York, New Jersey, Hawaii, Oregon, and others apply marginal tax brackets, similar to the federal system. California features the highest marginal bracket in the nation at 13.3%, alongside a mandatory State Disability Insurance (SDI) tax. New York applies SIT brackets up to 10.9% alongside state family leave (PFL) and disability deductions.

Form W-4 Withholding Options

In 2020, the IRS redesigned Form W-4, removing traditional "withholding allowances." The modern W-4 focuses on marital status, multiple jobs worksheets, child tax credits, and custom deductions.

If you have multiple income sources in your household, it is essential to coordinate W-4 forms across all employers. If you do not check the "Multiple Jobs" box in Step 2 of the form, both employers will apply a full standard deduction to your earnings, leading to under-withholding and a potentially large tax liability when filing your tax return.

Common Payroll & Withholding Queries

Clear, expert answers to key paycheck withholding, tax rate adjustment, and exemption questions.